The Evolution from Gen 8.5 to Gen 8.6 Panel Lines

2022-05-13

Key points

The summed capacity of Gen 8.5 TFT arrays, including TFT LCD, WOLED, QD OLED and RGB OLED panels, is larger than that of Gen 8.6 panel plants; However, most new panel plants are Gen 8.6 due to better cutting efficiency and OLED technology enhancements.

Why are Gen 8.6 TFT factories so popular, especially in China? Why don't new panel manufacturers just build traditional Gen 8.5 plants using glass substrate sizes that have been around for years? Is there a specific reason for the evolution from Gen 8.5 to Gen 8.6 panel lines?This is a topic that many equipment vendors have been discussing with panel manufacturers.

In the past two decades, the generation of TFT LCD (also expressed by the size of the glass substrate) has evolved from the first generation all the way to the tenth generation.

For reasons of product differentiation, process engineering and niche market targets, panel manufacturers have chosen special glass substrate sizes, derived from existing glass substrate sizes (e.g., Gen 7, Gen 8 and Gen 10 plants) and invented new generation sizes with small values (e.g., Gen 7.5, Gen 8.5 and Gen 10.5 plants). These particular derivatives have turned into mainstream plants due to significant investments and acceptance of these new sizes by new entrants in the TFT LCD market (for plant construction and capacity building).

The Gen 8.5 and Gen 8.6 lines are now the dominant factories with manufacturing capacity for TFT LCD, WOLED and QD OLED panels. The history and evolution of these generations of panel factories are shown in Figure 1.

The summed capacity of Gen 8.5 TFT arrays, including TFT LCD, WOLED, QD OLED and RGB OLED panels, is larger than that of Gen 8.6 panel plants; However, most new panel plants are Gen 8.6 due to better cutting efficiency and OLED technology enhancements.

Why are Gen 8.6 TFT factories so popular, especially in China? Why don't new panel manufacturers just build traditional Gen 8.5 plants using glass substrate sizes that have been around for years? Is there a specific reason for the evolution from Gen 8.5 to Gen 8.6 panel lines?This is a topic that many equipment vendors have been discussing with panel manufacturers.

In the past two decades, the generation of TFT LCD (also expressed by the size of the glass substrate) has evolved from the first generation all the way to the tenth generation.

For reasons of product differentiation, process engineering and niche market targets, panel manufacturers have chosen special glass substrate sizes, derived from existing glass substrate sizes (e.g., Gen 7, Gen 8 and Gen 10 plants) and invented new generation sizes with small values (e.g., Gen 7.5, Gen 8.5 and Gen 10.5 plants). These particular derivatives have turned into mainstream plants due to significant investments and acceptance of these new sizes by new entrants in the TFT LCD market (for plant construction and capacity building).

The Gen 8.5 and Gen 8.6 lines are now the dominant factories with manufacturing capacity for TFT LCD, WOLED and QD OLED panels. The history and evolution of these generations of panel factories are shown in Figure 1.

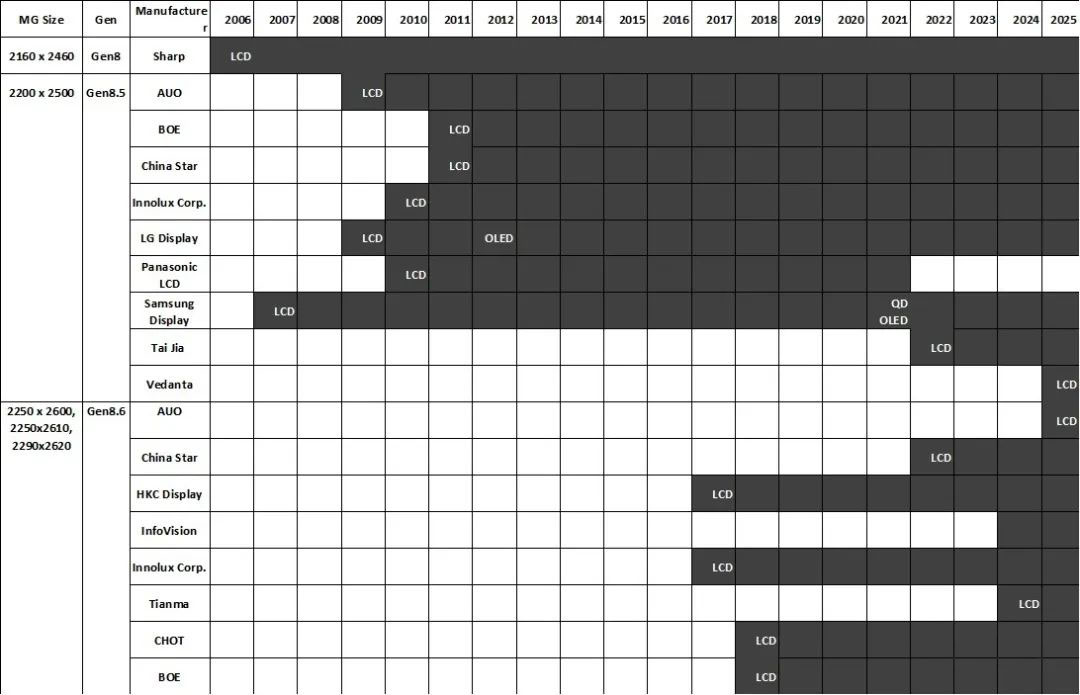

Figure 1: History of Gen 8, Gen 8.5 and Gen 8.6 TFT panel factories from 2006 to 2025

Note: "MG size" refers to the size of the master glass substrate

In 2006: the first Gen 8 factory

While Korean panel manufacturers like Samsung Display and LG Display, and Chinese Taiwan panel manufacturers like AUO and Chi Mei (later renamed to Innolux) chose Gen 7 (1870x2200mm) and Gen 7.5 (1950x2250mm) glass substrate sizes to produce 4x inch LCD TV panels with good economic cutting and panelization efficiency. However, Sharp has chosen a higher generation line to expand its glass substrate size to cut into larger TV panels.

Sharp is the first to launch an 8th generation line factory with a 2160x2460mm glass substrate. It is an extension of the Gen 7 line factory and can produce the following products.

32-inch panels, 18 pieces, with a cutting efficiency of 98%

46-inch panels, 8 pieces, with a cutting efficiency of 90%

52-inch panels, 6 pieces, with a cutting efficiency of 86%

60 or 62 inch panels, 3 pieces, features a cutting efficiency of 60%

60-inch MMG, 3 pieces, and 32-inch 3 pieces cut yields a cutting efficiency of 85%

This Gen 8 plant is the first of its kind in the world and is designed to compete with Gen 7-7.5 plants, which offer 12 cuts of 32-inch panels, 6 cuts of 46-inch panels, and 3 cuts of 52-inch panels. Sharp is at the forefront of LCD TV panel production, and its Gen 8 launch establishes a reference model for the coming years.

In 2007: Samsung Display's first Gen 8.5 line plant

Shortly after Sharp's Gen 8 plant achieved mass production, Samsung Display revamped the idea of the Gen 8 line by expanding its substrate size from 2160x2400mm to 2200x2500mm and renaming it "Gen 8.5 line".

Samsung Display started mass production of the following products at its Gen 8.5 plant.

32-inch panel with 18 cuts and 92% panel efficiency

46-49 inch panel, with 8 cuts and 85%-90% panelization efficiency

55-inch panel with 6 cuts and 91% panelization efficiency

65-inch panel with 3 cuts and 64% panelization efficiency

65-inch MMG with 3 cuts, and 32-inch 3 cuts with 94% panelization efficiency

With the new 8.5-generation line factory, Samsung Display can produce 46-49-inch panels to compete with 46-inch panels (similar cutting efficiency and depreciation costs), with 55-inch panels to compete with 52-inch panels (similar cutting efficiency and depreciation costs), and with 65-inch panels to compete with 62-inch panels.

The concept is to expand the glass substrate and reduce the space for process scribing to produce larger size panels to compete in the TV market (consumers are sensitive to both price and size).

Samsung Display's Gen 8.5 line factory gained immediate popularity and has been adopted by many panel manufacturers since 2007. LG Display and AUO began mass production of their Gen 8.5 TFT LCD plants in 2009, while Innolux (then known as Chi Mei) began mass production of its Gen 8.5 TFT LCD plant in 2010.

When TFT LCD panel manufacturers in mainland China decided to expand their production to Gen 8 and beyond, BOE and Huaxing Optoelectronics both chose Gen 8.5 plants to enter the LCD TV panel market. BOE's and Huaxing's Gen 8.5 line plants started operation in 2011.

From 2007-2017: The prevalence of Gen 8.5 lines and competition among 46, 47, 48 and 49 inch panels

During this decade, while Gen 8.5 plants did not move further into new generation lines, panel manufacturers continued to expand their Gen 8.5 line capacity; Gen 8.5 line plants became the mainstream of LCD TV panel production. 8.5 line TFT array capacity area also grew from 1.1 million square meters in 2007 to 135.7 million square meters in 2017.

Meanwhile, competition is fierce, especially for 46- and 48-inch versus 47- and 49-inch panels, which are produced in Gen 8.5 line factories.However, panel manufacturers compressed the space for panel design lines and processes to achieve sizes an inch larger than their peers. Samsung Display and AU Optronics started producing 46 inches, and then LG Display started producing 47 inches. Samsung Display reciprocated with 48 inches, while LG Display countered by increasing its panel size to 49 inches. Competition among Gen 8.5 panel manufacturers is harsh and widespread, but there is no doubt that 55-inch panels are becoming the dominant LCD TV size at 50 inches and above, as Gen 8.5 line factories promote the production of 55-inch panels.At the same time, LCD manufacturers in Mainland China use their 8.5-generation factories to produce a large number of 32-inch panels, driving the popularity of this panel size in the market.

In 2012: LG Display started production of WOLED for Gen 8.5 line

LG Display set a long-term goal to commercialize OLED TV panels with white OLED structures and oxide TFT back-planes. Starting in 2012,LG Display converted its TFT LCD production at its P8 plant (Gen 8.5 line with a glass substrate size of 2250x2600mm) to oxide TFT backplane and WOLED TV panel production. From 2012 to 2020, LG Display has been increasing its Gen 8.5 WOLED TV panel production capacity by integrating with its traditional Gen 8.5 TFT LCD capacity.LG Display also built a new 8.5-generation WOLED TV panel factory in Guangzhou, China in 2020. The company's WOLED TV panel production capacity soared to more than 7 million units a year.

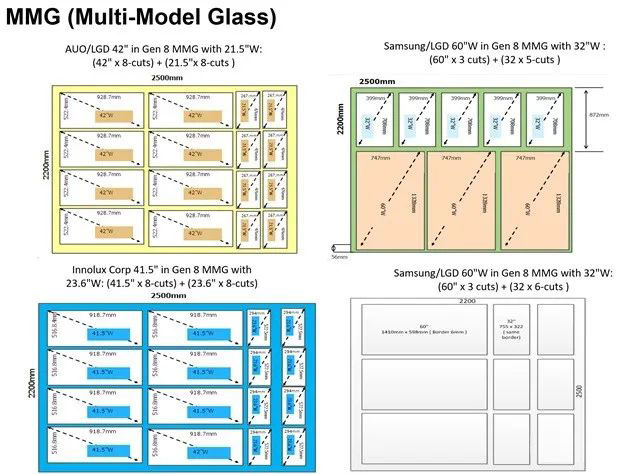

Starting in 2015: MMG for Gen 8.5 lines

MMG stands for Multi-Model Glass, meaning that panel manufacturers cut different sizes of panels on a single glass substrate. Since every panel manufacturer uses 8.5 generation factories, the competition becomes very homogeneous.Competition on price rather than product differentiation has changed panel manufacturers' thinking; They want to find solutions. Many MMG display panels were developed during this period, many of which are still in mass production today. Examples of these MMG display panels, all produced in Gen 8.5 plants, are as follows.

43-inch and 23-inch panels (Samsung display)

42-inch and 21.5-inch panels (AU Optronics and LG Display)

42.5-inch and 18.5-inch panels (BOE)

60-inch and 32-inch panels (Samsung Display, LG Display)

65-inch and 32-inch panels (Samsung Display,LG Display)

41.5-inch and 23.6-inch panels (Innolux, Huaxing)

65-inch and 55-inch panels (LG Display)

42.5-inch panel, 10 pieces cut in 8.5 generation factory (LG Display, BOE)

49-inch and 75-inch panels (LG Display)

An example of MMG is shown in Figure 2.

Figure 2: MMG in a Gen 8.5 plant

In 2017: Innolux developed 8.6 generation factories, followed by Huike

Intense competition among Gen 8.5 line products (such as 32-, 40 to 42-, 46 to 49- and 55-inch panels) spurred Innolux to change its thinking. It began to further expand its Gen 8.5 line glass substrates to promote larger panel sizes and avoid fierce competition while increasing demand for different sizes.

Innolux held talks with lithographic tool manufacturers (such as Canon) and photomask manufacturers to innovate the size of glass substrates;The idea for its Gen 8.6 line is to use a 2250x2600 mm glass substrate, which is slightly larger than the 2250x2500 mm glass substrate for the Gen 8.5 line. The length side of the glass substrate was expanded to produce a larger size panel here.

The 8.6 generation factory initiated by Innolux was later copied and carried forward by many LCD panel manufacturers in mainland China, gradually changing the size of LCD TV panels.

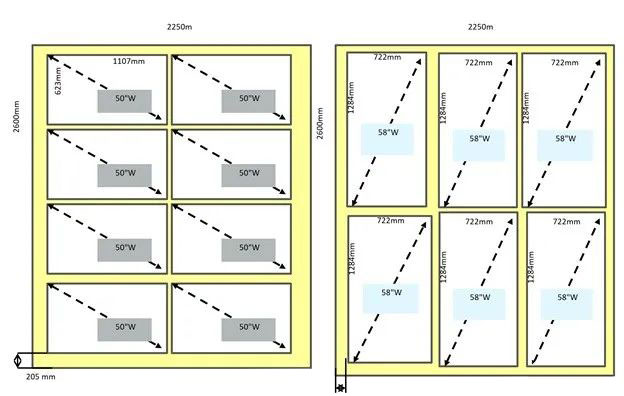

The Gen 8.6 plant produced display panels of the following sizes.

32-inch, 18 cuts, with a panelization efficiency of 87%

50-inch, 8 cuts, with apanelization efficiency of 94%

58-inch, 6 cuts, with 95% panelization efficiency

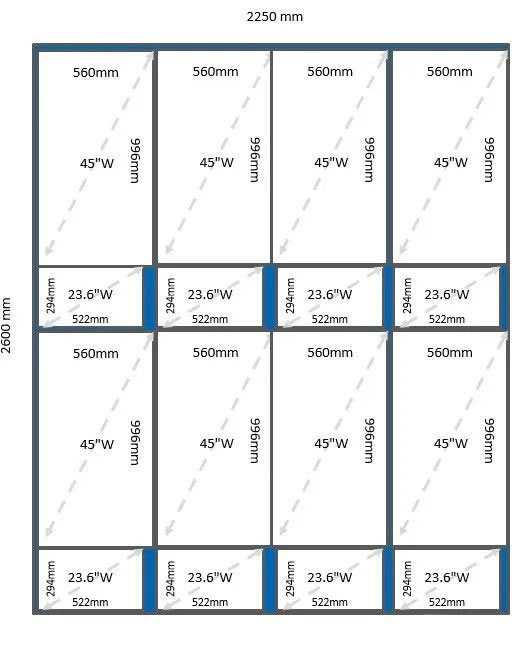

45-inch and 23.6-inch (or 21.5-inch) MMG with 8 cuts and 94% panelization efficiency

The 50-inch size of the Gen 8.6 factory was designed to compete with the 48- and 49-inch sizes of the Gen 8.5 factory. And the 45-inch size of the Gen 8.6 factory was designed to compete with the 42- and 43-inch sizes of the Gen 8.5 factory. As shown in Figures 3 and 4, the 58-inch size of the Gen 8.6 factory was designed to compete with the 55-inch size of the Gen 8.5 factory.

Figure 3: Production of 50- and 58-inch panels on Gen 8.6 line

Figure 4: 45-inch and 23.6-inch MMG produced on Gen 8.6 line

As a niche strategy company, Innolux's strategy paid off with the widespread acceptance of the 8.6 generation line factory.

Huike in mainland China soon followed Innolux's lead, and all Huike's Gen 8.x factories, from H1 to H5, were equipped with Gen 8.6 lines. Caihong Optronics' lead engineers also opted for Gen 8.6 lines. Innolux's Gen 8.6 line concept started in Taiwan, China, but has flourished in mainland China.

In 2018: new entrants in mainland China mimic the idea of making products above Gen 8.6 lines

With the popularity of 50-inch display panels, latecomers (Caihong Optronics, CEC Panda and others) in mainland China have followed with Gen 8.6 line plants. Both Caihong optronics and CEC Panda's new plants (later acquired by BOE in 2020) adopted the Gen 8.6 line concept; These companies built Gen 8.6 line plants instead of Gen 8.5 line plants.

Due to various design rules and panel design space, some panel manufacturers have even developed various derivative glass substrate sizes for Gen 8.6 plants, including 2250x2610 mm and 2290x2620 mm glass substrate sizes; These are referred to as "Gen 8.6+". Some panel manufacturers have even come up with the idea of 2300x2700 mm substrate sizes, called "Gen 8.7 lines," to produce 65- and 75-inch products to compete with Gen 10.5 line plants. In the end, the idea of a Gen 8.7 line did not come to fruition.

These activities are shown in Tables 1 and 2.

Table 1: Gen 8, Gen 8.5, Gen 8.6, and Gen 8.6+ Factories in 2018

Table 2: Gen 8, Gen 8.5, Gen 8.6, and Gen 8.6+ Factories and their cutting efficiency

The prevalence of 8.6 generation line factories helped the 50-inch size beat out the 46-49-inch size segment to become the mainstream LCD TV panel size.

Government support is also beneficial for the Gen 8.6 factories; it is easier to convince the government to build a new Gen 8.6 factory than to build an old Gen 8.5 factory. Therefore, when new entrants applied for government support to build new factories in China, they convinced the government with an Gen 8.6 plant instead of an Gen 8.5 plant.

Production of Gen 8.6 LCD panel plants continues to grow; the capacity of Gen 8.6 plants has grown from 5.1 million square meters in 2017 to 69.4 million square meters in 2022. It is expected to grow further to 122.9 million square meters in 2025.

From 2019 to present: shifting some Gen 8.5 line capacity to IT panels

The Gen 8, Gen 8.5 and Gen 8.6 plants were originally designed for LCD TV applications. However, panel manufacturers see the following reasons for producing IT panels (including desktop, notebook and tablet panels) in the Gen 8.5 or Gen 8.6 plants.

Good glass substrate cutting efficiency

Coping with the risk of oversupply of LCD TV panels

Stable demand for notebook and LCD desktop monitor panels, while demand for LCD TV panels is highly volatile; IT panels are also less price sensitive

In response to new panel size trends (e.g., larger desktop and notebook panels) and new aspect ratios

Shifting more LCD TV panel production to Gen 10.5 plants, thereby dedicating capacity from Gen 8.5 or 8.6 plants to IT panel production

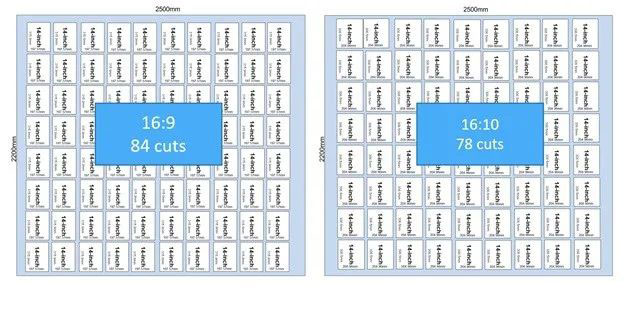

One example is the so-called new 16:10 aspect ratio laptop panel; These panels cost 10-20% more than 16:9 panels.

Demand for 16:10 laptop panels is growing rapidly and outpacing the demand for 16:9 laptop panels. This is because of the rising trend of multiple screens at work.

Due to lower production efficiency and glass utilization, 16:10 panels are more expensive than traditional 16:9 products. The lower production efficiency leads to higher costs for panel manufacturers. Additional costs are also incurred if the 16:10 panel uses a special T-con and display driver chip (DDIC). When producing 16:10 laptop panels in different generation line factories, the cutting efficiency of 16:10 panels is 10%-20% lower than 16:9 panels. Also, if the 16:10 panel has IPS wide viewing angle, 250 nits high brightness, low power consumption, low blue light and ultra-light backlight panel, the cost premium will increase.

Table 3: 14-inch panelization (cutting) and cost premiums by generation line plant

Figure 5: Comparison of 14-inch 16:9 and 16:10 panels in Gen 8.5 plants

2021-2022: Samsung Display converts its Gen 8.5 LCD factory to a Gen 8.5 QD OLED factory

Starting in 2018, Samsung Display has gradually withdrawn from the LCD panel business by sequentially restructuring its legacy LCD factories. Some of its Gen 8.5 LCD capacity has been modified and amended to produce QD OLED (or so-called Quantum Display) panels.

Samsung Display's Q1 factory is the world's first Gen 8.5 line QD OLED factory (it is Samsung Display's converted legacy Gen 8.5 line LCD factory.) The Q1 factory had a trial run in the fourth quarter of 2021 and began mass production of 55- and 65-inch QD OLED TV panels and 34-inch QD OLED desktop display panels in the first quarter of 2022. Meanwhile, a new company in China, Taijia Optoelectronics, purchased obsolete equipment removed from Samsung's display Gen 8.5 plant and reloaded the equipment into China. In India, Vedanta announced plans to invest in the country's first Gen 8.5 TFT LCD factory.

2023 ~: New 8.6 generation line LCD and OLED panels for IT products

As LCD TV panel capacity has been quite sufficient and IT panel demand has been strong for a long time, panel manufacturers have started to plan new 8.6 generation line factories for IT panels and OLED panels. Their plans are as follows; Some are already in the construction stage, while others are still in the planning and evaluation stage.

Huaxing's T9 TFT LCD plant: The Gen 8.6 plant is used for IT panel production, using amorphous silicon and oxide TFT LCD technology. The plant is scheduled to start putting in glass substrates from the fourth quarter of 2022.

Tianma's TM19 TFT LCD plant: The Gen 8.6 line plant is for IT panel production, using amorphous silicon and oxide TFT LCD technology. Planning for this plant is underway.

Konka's K2 TFT LCD plant: The Gen 8.6 line plant is for IT panel production, using amorphous silicon and oxide TFT LCD technology. The plant is under feasibility study.

BOE's B16 Gen 8.6 OLED plant in Chengdu, China. The plant is undergoing feasibility study.

Samsung's new Gen 8.5 OLED plant: a Gen 8.5 plant for OLED IT panel production. The plant is under planning.

AUO's new Gen 8.6 or Gen 8.7 LTPS and Oxide composite TFT LCD plant in Taiwan, China, for IT panel production and also for Micro LED. The plant is under planning.

In summary, we can consolidate the history of the Gen 8.5 and Gen 8.6 plants as follows.

2006: Sharp's first Gen 8 plant

2007: Samsung Display's first Gen 8.5 line factory

2007-2017: Prevalence of Gen 8.5 line factories and competition between 46, 47, 48 and 49 inches

2012: LG Display starts to produce Gen 8.5 WOLED panels

2015 onwards: MMG for Gen 8.5 line

2017: Innolux launched the idea of Gen 8.6 line, followed by Huike

2018: New entrants in mainland China market imitate the idea of Gen 8.6 lines

2019-present: Some Gen 8.5 line capacity is shifted to IT panels

2021-2022: Samsung Display converts its Gen 8.5 LCD plant to a Gen 8.5 QD OLED plant

2022: New Gen 8.6 LCD and OLED plants for IT products

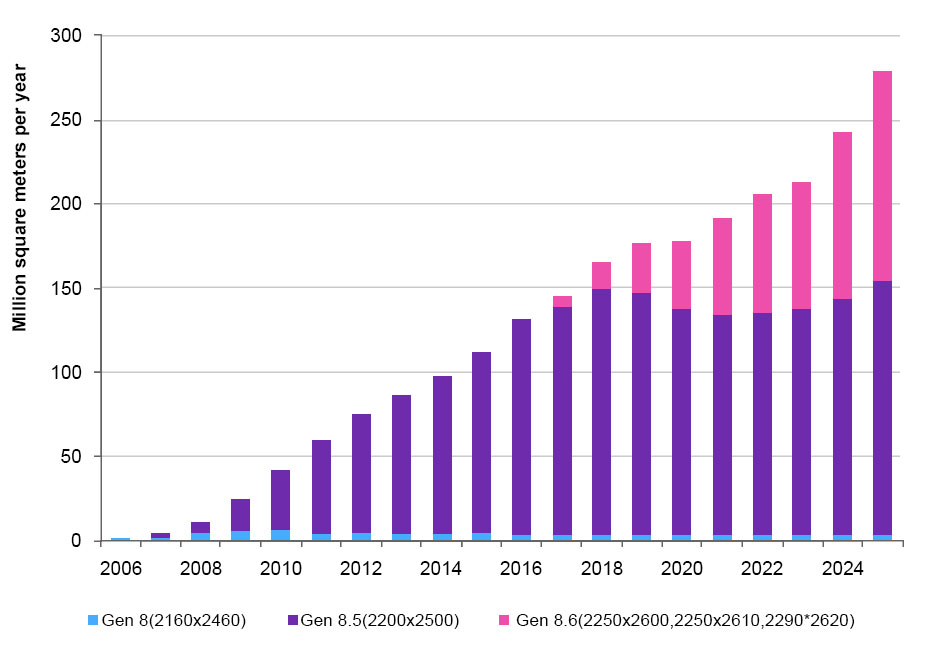

Gen 8.6 is the present and the future. In terms of capacity, Gen 8.5 TFT capacity (including LCD, WOLED and QD OLED) is still larger than Gen 8.6; however, the expansion of Gen 8.6 plants is more robust.

Gen 8.5 capacity declines from 2019, mainly due to restructuring of panel manufacturers such as Samsung Display and Panasonic LCD, as well as capacity restructuring at LG Display's Gen 8 plant. However, Gen 8.5 line capacity will gradually pick up from 2023 due to new capacity in WOLED and QD OLED panels, as well as capacity from Vedanta in India and Taijia Optronics in China.

Gen 8.6 line TFT capacity, including TFT LCD, WOLED, QD OLED and RGB OLED panels, is expected to grow from 38.9 million square meters in 2020 to 122.9 million square meters in 2025.

Therefore, in 2025, the TFT array capacity of Gen 8.5 and Gen 8.6 lines will be 151.2 million square meters and 122.9 million square meters, respectively.

Figure 6: Gen 8, Gen 8.5 and Gen 8.6 TFT capacity (including LCD and OLED)

X

We use cookies to offer you a better browsing experience, analyze site traffic and personalize content. By using this site, you agree to our use of cookies.

Privacy Policy